Australia’s mining thirst: the gas to liquid solution

By SS Shastri, SF Kamper, TR Sonigra, TR Hill and J Beales, GHD Pty Ltd

Wednesday, 19 September, 2012

The iron ore industry in Western Australia consumes in excess of a 3 million litres of diesel each day. This diesel is delivered to the mine sites either by rail up to the site load-out or by a combination of rail and road. The use of mine transport corridors for transport of fuel not only adds significant costs, but also has a considerable safety impact.

Australia is currently heavily dependent on road transport for the movement of goods across the country. The primary fuel that drives this aspect of the economy is diesel. Diesel, too, is the lifeblood of the mining industry from providing power to facilities and accommodation to heavy haulage and everything in between. It is predicted that diesel fuel usage will continue to grow with the global demand for Australian resources and domestic consumption.

Australia currently imports about a third of its liquid fuels; a continued increase in fuel imports is neither sustainable nor acceptable. It may be argued that Australia’s access to international markets suggests that energy security may be good; however, Figure 1 shows that Australia’s self-sufficiency is reducing. There is therefore a real opportunity to grow local industry and increase energy security.

Australian natural gas reserves (including coal seam methane and shale gas) are significant and new discoveries are being made. Gas reserves close to the coast and major infrastructure hubs can be transported and processed relatively cheaply compared to LNG or other products. Stranded gas reserves on the other hand are stranded by virtue of being economically too far away from gas processing and transfer infrastructure.

While some new shale and tight gas locations are potentially stranded, many of these reserves are close to or overlap some of the active mining tenements. In Western Australia, for instance, potential shale gas reserves are located close to the Pilbara where most of Australia’s iron ore is being produced.

With the iron ore industry in Western Australia consuming in excess of 3 million litres of diesel each day, there is a case for the use of this stranded gas not only to meet the power requirements of the mines located in their neighbourhood, but also the significant liquid fuel requirements of the mines. This can be achieved through small-scale conversion of natural gas to diesel fuel through the well-understood gas to liquid (GTL) process.

Location of mines and shale gas reserves

Australia has a number of shale and tight gas basins such as Cooper, Amadeus and Georgina, among others. The Amadeus Basin is the closest to the Pilbara mining infrastructure, and companies are beginning exploration activity in this basin. A portion of the Amadeus Basin has already been explored and there is a pipeline to NT. Other shale and tight gas deposits are to be explored (eg, Central Petroleum’s reserves).

Central Petroleum’s stake in the Amadeus Basin, for instance, has an estimated 26 trillion cubic feet of gas - a potentially significant resource.

The iron ore mines are located almost midway between the coast and the shale gas basins to the east. Until the global supply of LNG exceeds demand, economics favour export over domestic use. Existing gas processing infrastructure on the coast may have insufficient capacity to process additional gas. Should processing capacity exist in infrastructure on the coast, the cost of laying a new pipeline across several active mine sites may be cost prohibitive.

Gas geographically close to Pilbara mine sites increases the potential for commercial exploitation by both the miners and gas producers.

Gas to liquid process

Gas to liquid refers to the conversion of natural gas to a hydrocarbon liquid fuel (crude) that can be converted to diesel or other final fuel.

The GTL process is an established process with a long history. Figure 2 depicts the process. Natural gas (primarily methane) is reformed with steam to produce synthesis gas (molar ratio of hydrogen to carbon monoxide of 2 to 1). The synthesis gas is then converted by Fischer Tropsch (FT) reaction to synthetic crude oil that is further refined to produce middle distillates or diesel.

The details of the Fischer-Tropsch process are covered by a significant body of knowledge spanning several decades that is available in journals and books.

There are a number of current research projects aimed at reducing the costs of the GTL process. For example, CSIRO in Australia has research projects aimed at reducing the energy usage in the synthesis gas formation step of the process and aimed at finding a catalyst to target diesel production over other hydrocarbon formation. Both projects (if successful) will reduce the costs of the plant2.

Proposal and technical feasibility

Demand rationale

In Australia, 40 companies in the mining sector consumed 52.5 PJ of diesel equivalent in 2008-093. The heating value of diesel ranges between 44 and 48 MJ per kilogram and density ranges from 820 to 860 kg/m3. Assuming a mid-value for heating value and density, this energy represents 8.9 million barrels consumed in 2008-09 for mine production, including 342 million tonnes of iron ore in Australia. The current production of iron ore is 408 million tonnes and simple extrapolation would indicate a diesel consumption of about 10 million barrels. However, personal communication with a senior mine executive indicated that 1 million litres of diesel is consumed each day to meet a production target of nearly 15% of overall iron ore output (this is consistent with published literature). This equates to about 42,000 barrels of fuel consumption a day. As no mining operation will provide exact data on fuel consumption, it is reasonable to assume that diesel consumption will be somewhere between 10 and 15.3 million barrels each year.

Over 2011, the base cost of diesel has hovered between 70 and 80 cents per litre; with shipping costs this increased to between $1.20 and $1.30 per litre. With other additions, the final retail price of diesel (including all costs and taxes) varied between $1.30 and $1.605. It is understood that this final retail cost is based on import pricing parity, and large mining customers and the agricultural sector could get discounts of the order of 30%. Therefore, cost at source (gate) is assumed to be $1.45 (average of high and low retail) discounted by 30% to $1.015 a litre. The actual transportation costs to the point of use, sometimes several hundred kilometres away, are not known. The past year has seen the steady increase in fuel prices, and in early December 2011, West Texas Intermediate crude was selling at around $100 a barrel.

The current cost of diesel in terms of energy is about $27 per GJ (this may or may not include transportation costs to site and is the gate price). The cost of gas delivered to the Sino Iron Ore project, for example, is between $11 and $13 per GJ6. Thus inclusive of pipeline costs, cost of gas appears to be between 2 and 2.5 times less than that of diesel.

Safety rationale

The delivery of diesel fuel to the point of use often requires the use of other infrastructure - road and rail primarily. The use of road infrastructure implies sharing of roads with other users, light vehicles, heavy haul trucks (some up to five cars) and sometimes dump trucks. Segregation of traffic is not always possible and in a mine environment a major hazard is the non-segregation of traffic that could lead to vehicle interactions. From a rail perspective, the need to send a fuel rake on a shared line is in itself not a problem as most rail operations in Australia are very tightly regulated; however, it does bring in a scheduling constraint, as most mining operations are poised to grow significantly.

Transportation rationale

The scheduling of fuel transport either by rail or road reduces overall capacity available for resource transfer; and based on current expansion plans, it appears that existing infrastructure will be used to near capacity.

Large operators such as Rio Tinto and BHP Billiton have gas supply infrastructure to some of their facilities; for example, the Goldfields Gas Transmission (GGT) pipeline delivers gas to Rio’s operations in Paraburdoo. This gas is presently consumed to produce power for the mines and local communities.

Environmental benefits

There are significant environmental benefits to producing GTL (synthetic) diesel close to the point of use. The environmental impact of transporting diesel from Singapore to Australia, and then onwards to the mining areas, will be significantly lessened. Catalyst from the FT process plant is recyclable and the resulting water product can be used for irrigation or within the mining process.

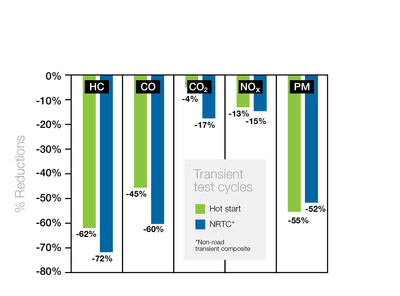

GTL diesel will have a better environmental and performance profile than conventional diesels derived from crude oil. The diesel is characterised by a high cetane number (at least 70), low sulfur (less than five parts per million), low aromatics (less than 1%) and good cold flow characteristics (less than 5-10°C). Figure 3 is taken from the Hobbs report to the Southern States Energy Board, Georgia titled American Energy Security7.

Synthetic GTL diesel is compatible with existing fuel distribution infrastructure. In addition, GTL diesel can be used in both current and envisaged future diesel engines, along with their exhaust gas after-treatment technologies; meaning few (if any) modifications to existing equipment and infrastructure are required to realise the benefits.

Cost analysis

A typical operation would consume about 1 million litres of diesel each day (~6000 barrels) and some of the larger operations would consume a little over 1.6 million litres of diesel each day (~10,300 barrels); therefore, a gas to liquids facility to produce 10,000 barrels of diesel per day is considered for this analysis. Based on a material balance (Marano and Ciferno, 20018), a 17,000 barrel per day GTL facility will produce approximately 10,000 barrels of diesel per day.

CAPEX

Pacific GTL’s proposed 17,000 barrels per day was estimated to cost $1.5 billion in 2010, and was to have been located in Brisbane. Assume therefore that this size plant built in the Pilbara will cost $2.0 billion. With constant advances in catalyst technology and the use of clever modularised design and construction it would be hoped that this cost could be reduced.

Factors that need to be taken into consideration are lead times required for design and construction and the need for speed of delivery to match planned growth. It may be worth considering off-the-shelf technologies that would be suited to a range of production capacities ranging from 200 to 5,000 barrels per day.

OPEX

A 17,000 barrels/day GTL plant would require about 9 TJ/day of gas; based on pricing for which data is available ($11/GJ) this would equate to $100,000 a day for gas, or $10 per barrel of diesel. The cost of producing the diesel is estimated (internal calculations) to be about US$23 a barrel, which equates to about 15 cents per litre or, based on 10,000 barrels a day, equals $230,000 per day.

The current cost of purchasing commercial diesel at gate prices is estimated to be about US$1.6 million a day (based on 10,000 barrels a day at $1.015 per litre) and over a year US$584 million. This cost does not include the cost of transport to site, safety costs, scheduling costs and additional infrastructure required such as large tank farms and distribution facilities. For the purposes of the calculation, an additional 10c per litre have been added, actual data is required to improve this accuracy.

Return on investment

The cost analysis considered the construction of a 17,000 barrels per day gas-to-liquid facility. The model assumed three years for the design and construction of the facility. No credit is taken for either electric power produced by the GTL process or for the LPG/gasoline that is produced. For ease of calculation (as this indicative only), the price of fuel and operating costs remain unchanged over 10 years. Under these conditions the break-even point is reached 10 years from the time the funds are sanctioned. At the end of 20 years, the IRR is 10%.

The GTL process produces other saleable hydrocarbon products as well as diesel. The potential revenue from these has not been taken into account in the economic analysis for this article; it would be expected to have a positive impact on the returns from the project, however.

The construction of a GTL facility as a collaborative venture between a large operator and a stranded gas developer could result in cost savings of nearly 85% in actual fuel costs and a positive return on investment in less than 10 years. When the significant amount of research into this technology begins to bear fruit, it is likely that the economic returns from the investment will be greatly increased.

References

- ACIL Tasman, An assessment of Australia’s liquid fuel vulnerability, November 2008

- CSIRO Report, Gas Processing and Conversion: fuel for Australia's future, http://www.csiro.au/en/Outcomes/Energy/Gas-Processing-Conversion-Fuel-Future.aspx, accessed 01 February 2012

- Australian Government, Department of Energy and Tourism, EEO Case Study - Analyses of diesel use for mine haul and transport operations, 2010

- Ocean Equities African Iron Ore Sector Research 07072011, Iron Ore Sector update, downloaded 13 Dec 2011 from http://www.sundanceresources.com

- http://www.aip.com.au/pricing/facts/Weekly_Diesel_Prices_Report.htm, fuel pricing details, accessed 8 Dec, 2011

- ACIL Tasman, Gas prices in Western Australia, May 2010

- The Southern States Energy Board Norcross, Georgia, American Energy Security - Building a bridge to energy independence and to a sustainable future, July 2006

- Marano JJ and Ciferno JP, Life-Cycle Greenhouse-Gas Emissions Inventory for Fischer-Tropsch Fuels, Energy and Environmental Solutions paper for US Dept. of Energy, National Energy Testing Laboratory, June 2001

Australia's green metals gambit: the technologies to decarbonise steel

A renewables-driven revolution in mining and metals processing could supercharge Australia's...

Australian manufacturers should prioritise energy optimisation over net zero

Energy efficiency consultancy DETA Consulting says Australian manufacturers need to fix the...

The US market opportunity Australian engineering firms need right now

Australia is in the midst of an engineering talent crisis, but recuiting graduates from the US...

")